Today the House Committee on Economic Development passed economic development bill HCS SB 8 by 21-4 vote. Included in the bill, to be considered by the full House as soon as tomorrow, would be major and devastating changes to the state’s historic rehabilitation tax credit as well as changes to the low income housing and distressed areas land assemblage tax credits.

Here are excerpts from the official substitute summary.

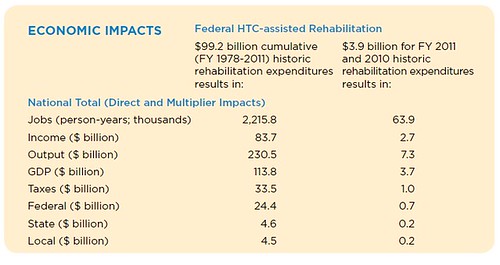

Historic Rehabilitation Tax Credits

For each fiscal year beginning on or after July 1, 2011, the substitute limits to $80 million the total amount of credits that the Department of Economic Development can approve.

For all applications for credits approved on or after July 1, 2011, no more than $125,000 may be issued for eligible costs and expenses incurred in the rehabilitation of certain eligible owner-occupied residential property.

For each fiscal year beginning on or after July 1, 2011, the substitute limits to $10 million the total amount of credits for projects receiving less than $275,000 that the Department of Economic Development can approve.

For all credits authorized on or after July 1, 2011, the substitute reduces from three years to one year the time period that the credit can be carried back and from 10 years to five years the time period that the credit can be carried forward.

A taxpayer who receives a low-income housing tax credit for a project not financed through tax-exempt bond issuance cannot be eligible for a historic preservation tax credit for the same project.

An application for final approval and issuance of a tax credit must include a cost and expense certification by an independent licensed certified public accountant with any accrued developer fees stated separately. The department will have 120 days from receipt of the application for final approval to determine whether the completed project meets required standards and to issue tax credit certificates equal to 75% of the eligible costs and expenses verified to that date. If a taxpayer receives tax credits that include an amount attributable to accrued developer fees, he or she must submit within six years of completion of the rehabilitation an additional cost and expense certification verifying the total amount of developer fees actually accrued and paid. If the amount of the tax credits issued and attributable to developer fees exceeds the amount of developer fees actually accrued and paid, the taxpayer is liable to repay 25% of the excess. A taxpayer or his or her authorized representative may appeal any official decision on a preliminary or final approval to an independent third party appeals officer designated by the department.

Low Income Housing Tax Credit

For each fiscal year beginning on or after July 1, 2011, the substitute limits the total amount of low income housing tax credits that can be authorized for projects not financed through tax exempt bond issuance to $110 million, authorizes the tax credit to be carried forward for five years, and reduces from three years to two years the time period that a low income housing tax credit can be carried back.

Beginning July 1, 2011, the substitute limits the total amount of low income housing tax credits that can be authorized annually for projects financed through tax exempt bond issuance to $20 million.

Distressed Areas Land Assemblage Tax Credit

This substitute expands the definition of “eligible project area” for purposes of the distressed land assemblage tax credit program to include a “redevelopment area” as defined in the real property tax increment allocation development act that contains at least 300 acres in 80 or more parcels, includes or previously included in excess of 10 million square feet of commercial building space, and is located within a “low income community” as defined in 26 U.S.C. Section 45D.

The five year restriction during which an applicant can receive a tax credit for all interest costs under the act is removed. Engineering costs, attorney=s fees, and architectural and planning costs are now authorized “acquisition costs”, and the allowable tax credit for demolition costs is increased from 50% to 100%. An applicant can file for the tax credit quarterly rather than annually.

The annual program cap is increased from $20 million to $30 million, although the aggregate program cap remains at $95 million. A process is established for allocating the annual $30 million in tax credits, depending upon the number of eligible applicants, provided however that if there are more than two applicants, no single applicant can receive more than 50% of the available tax credits. The sunset date is extended from August 28, 2013, to August 28, 2016.